AI has already found its way into accounting, from automated reporting tools to email assistants that save you hours of typing. But in a field built on trust, privacy, and compliance, speed alone isn’t enough. The question isn’t if accountants should use AI, but how to use it without crossing any red lines.

This guide helps you better understand the role of AI in accounting. You’ll see where AI can safely lighten your workload today, and where caution (and the right systems) is non-negotiable. You'll discover some quick wins you can grab right now, plus advanced use cases you can explore once your vendors tick the boxes for security and compliance.

👉 By the end, you’ll know exactly which AI shortcuts are safe to take, and which ones need a 'proceed with care' sign.

Key considerations for AI in accounting

Many firms get overwhelmed with AI. Some go all-in so fast that they forget about the practicalities. In plenty of industries, that overuse is mostly harmless. In accounting, it isn’t. AI still isn’t fully harmonized in law, and the wrong tool or sloppy workflow can leak confidential data or mislead clients.

At the same time, the profession is clearly moving: in a 2025 survey, 46% of accountants reported using AI daily, 81% said it improved productivity, and two-thirds admitted they feel overwhelmed by tech complexity at least weekly.

Translation: adoption is up, governance is lagging.

Security

Client ledgers, payroll files, bank feeds: this is high-value data.

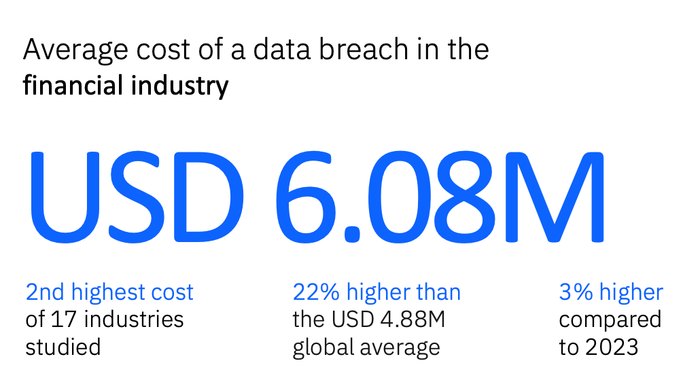

Attackers know it, and the costs of mistakes are real. IBM’s 2024 breach study put the global average breach at $4.88M, and financial-industry breaches were even higher at $6.08M on average.

For firms, 'move fast and break things' is not a strategy. You should insist on strong encryption (in transit and at rest), granular access controls, and vendors with SOC 2 attestation and/or ISO/IEC 27001 certification. SOC 2 evaluates controls across security, availability, processing integrity, confidentiality, and privacy; ISO 27001 sets requirements for running a robust information security management system. Ask for current reports/certificates, scope, and any exceptions.

To protect sensitive data while still leveraging AI, use tools built for compliance. For example, Maxio’s subscription billing software provides secure handling of recurring revenue streams.

Data privacy

Accounting records often bundle PII with financial identifiers, and many client relationships sit under NDAs.

That creates two immediate rules of thumb: don’t paste sensitive client data into consumer AI and minimize data you share, even with enterprise tools.

If you do use AI with client information, document your lawful basis, data-minimize, anonymize/pseudonymize where possible, and control cross-border transfers. Under GDPR, organizations must collect, store, and process personal data with clear purposes and safeguards; the UK ICO’s guidance adds detailed expectations around transparency and accuracy for AI systems.

Build prompts that avoid IDs, names, and amounts unless your platform is contractually 'no-train,' encrypted, and access-restricted.

Compliance & standards

AI doesn’t replace GAAP/IFRS discipline; it sits beside it. Any AI-assisted conclusion should remain explainable and reconcilable to source documents, with no 'black box' numbers. Keep an audit trail that shows the underlying data, the prompt/parameters, the model version, and your review notes.

In the EU, the AI Act is phasing in: it entered into force on 1 Aug 2024; prohibitions and AI-literacy duties applied from 2 Feb 2025; governance rules and obligations for general-purpose AI models became applicable 2 Aug 2025; most obligations become fully applicable 2 Aug 2026 (with extended transition for certain high-risk systems). Even if the tool you want to use isn't 'high-risk,' the direction of travel is clear: more documentation, testing, and transparency.

Human oversight

AI is a powerful tool, but it’s not foolproof. Models still hallucinate or misread context, especially when prompts bundle edge cases.

Keep a qualified professional in the loop for any client-facing output and for every material judgment.

Maintain a two-step review for numbers:

- source check (tie back to the ledger)

- and sanity check (does the result make business sense?).

On disclosure, U.S. CPAs don’t currently face a specific federal rule that mandates telling clients when gen-AI is used, but guidance points to a patchwork – meaning firms should decide, document, and communicate a consistent stance (for example: 'We may use AI to draft communications; humans review all outputs; we never feed confidential data into public models').

Secure the stack, minimize data exposure, keep outputs explainable, and never skip human review.

With those guardrails, you get the upside – speed and clarity – but without trading away trust.

6 AI practices that accountants can safely use today

Not every AI tool needs to come with a disclaimer or a legal review. In fact, there’s a whole set of uses that are completely safe because they don’t touch client records or cross compliance lines. They can make your day lighter without raising privacy flags. Better yet, many of these can be done with free tools you already have on your desk, or features tucked into platforms you’re using anyway, like Capsule CRM.

Here’s where you can start experimenting with AI today, risk-free.

#1 Drafting client emails with AI assistants

Email is the accountant’s never-ending task. AI can take the edge off by helping you draft messages faster, while you stay in full control of what gets sent. The golden rule: never feed in sensitive client data. Keep prompts generic, then add the details yourself before hitting send.

Here are five safe ways to use AI for email drafting:

- Gentle payment reminders – friendly nudges without awkward phrasing.

- Scheduling or rescheduling appointments – clear, polite coordination emails.

- Welcoming a new client – a warm onboarding message with next steps.

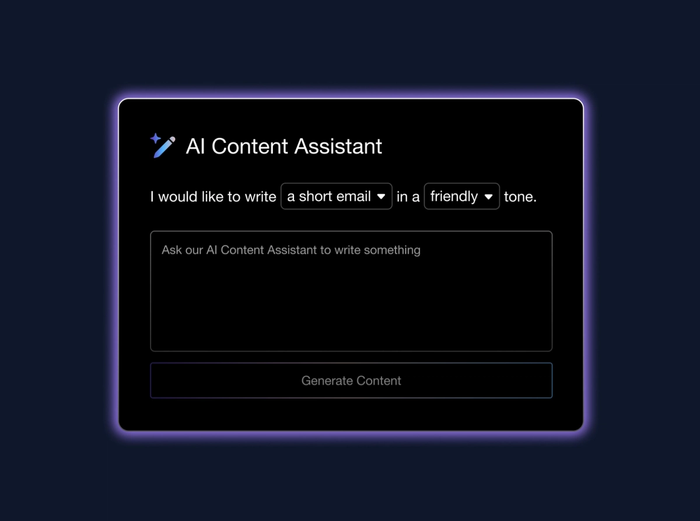

Capsule’s AI Content Assistant makes this painless. It helps you unblock writer’s block by generating quick, relevant email drafts in seconds.

You set the tone and topic, the AI drafts the copy, and you polish it as needed. Simple as that. And, it’s built right into Capsule CRM, so you don’t need extra tools or technical know-how.

👉 Safe, fast, and human-checked — that’s how AI belongs in your inbox.

#2 Summarizing public regulations or standards

For many in the accounting profession, the real challenge isn’t finding new tax laws or IFRS updates – it’s turning them into something clients can actually understand. These documents are public, which means there’s no data security risk in asking AI to process them.

With generative AI tools, you can feed in a new tax bracket update, tax return preparation, and implications for cash flow, or regulatory notice and get a clear, client-friendly summary in seconds.

This is especially useful when clients flood your inbox with questions. Instead of sending them a link full of technical language, you can prepare a concise explanation of what changed and why it matters. That saves your accounting team hours of manual data entry or repetitive tasks, while improving the overall quality of business communication.

#3 Automating meeting agendas and notes

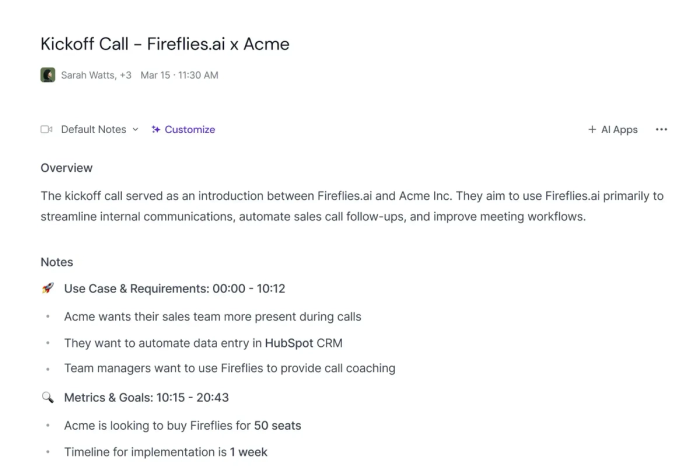

Meetings eat into time that could be spent on client service or analyzing accounting data. AI can help lighten the load by generating agendas from discussion topics or summarizing transcripts. Tools like Fireflies, Otter.ai, or built-in assistants in collaboration platforms can capture the conversation and turn it into structured action points.

This is a low-risk use of accounting AI, as long as you keep sensitive numbers or confidential details out of the transcripts.

There's one important yet often overlooked aspect to that, though. You should always get explicit consent from clients, stakeholders, or employees before recording. A simple 'this call is being recorded for notes' protects trust and keeps you compliant with privacy standards.

For modern accounting firms, automating this routine task reduces manual note-taking and improves accuracy – especially if you take a lot of calls daily, or need to pass the info to more people in your team.

#4 Internal knowledge search and FAQ drafting

Every accounting practice develops a ton of know-how, from categorizing financial transactions to preparing financial reports. The problem? It’s usually buried in thousands of emails or siloed in someone’s head. AI can help you turn this chaos into clear internal guides and FAQs without ever touching client data.

Here’s a simple 5-step way to do it safely:

- Collect your unstructured data. Gather notes, checklists, or process docs (e.g., how to process expense reports).

- Feed the AI only safe content. Upload internal guidance, never confidential client records or financial statements.

- Ask AI to organize the material. Example prompt: 'Turn these notes into a step-by-step guide for invoice processing.'

- Review and validate with human expertise. Make sure outputs align with your actual accounting processes and remove mistakes.

- Publish as an internal FAQ or guide. Store it in knowledge management tools like Guru or document management system so your accounting team can access it anytime.

This approach reduces repetitive questions and helps both large and small accounting firms keep their accounting data organized. AI handles the clustering of structured data while you provide the oversight. Win-win.

#5 Creating training materials for staff

Once you’ve organized your internal knowledge base and FAQs, the next step is making that content actionable for your team. Many firms have strong client processes but stumble on staff training. New hires face steep learning curves, and experienced accountants need refreshers as standards evolve.

AI support can bridge this gap by transforming your structured know-how into consistent, easy-to-use training materials.

Here are six safe ways to put AI to work in training:

- Onboarding playbooks with structured introductions to firm culture, tools, and workflows.

- Compliance checklists with tailored guides for financial audits and regulatory requirements.

- Interactive quizzes with quick tests that help spot knowledge gaps and prevent human error.

- Practice datasets with anonymized historical data that staff can use for mock analyses.

- Policy breakdowns with simplified versions of dense HR or compliance docs.

- Trend updates with bite-sized lessons on future trends shaping the accounting profession.

Unlike client-facing tasks, this is a no-risk zone: you’re not exposing accurate financial records, just repurposing internal knowledge into formats that make continuous training far less of a burden.

#6 Improving client communication tone

Accounting professionals know the struggle: you draft a perfectly accurate message, only to realize it sounds like it was written for an audit committee instead of a client. AI can help smooth out the tone by rephrasing complex accounting jargon into plain English.

This is also useful when emotions run high. Say you’re dealing with a very upset client. While you might feel like firing back defensively, AI can help you reframe the message using nonviolent communication (NVC) principles, turning a tense exchange into constructive dialogue.

Here’s how that looks in practice:

Without NVC (raw draft):

'Your delayed payment is holding up the audit process. If this continues, we won’t be able to finalize your financial statements on time.'

With NVC (AI-assisted tone):

'I understand the delay may be challenging on your end. To keep the audit process on track and deliver your financial statements as scheduled, we’ll need to receive the payment soon. Please let me know if there’s anything blocking this on your side.'

AI can also be a 'tone pacifier' for handling sales objections or following up without sounding robotic.

For accountants who don’t want to spend half an hour rewording a sensitive email, this is one of the safest, most impactful applications of AI technology in client communication.

7 accounting AI practices under consideration

Not every AI use case is safe to try out with free tools. Some applications touch highly sensitive accounting data, meaning they should only be explored in a regulated environment with secure, compliant systems. AI is powerful enough to help with all of the practices below, but it comes with responsibility. Usually, these solutions are only available inside enterprise-level platforms, not in consumer-grade apps.

If you experiment outside of that environment, you do so at your own risk.

Invoice scanning and categorization

AI can automate routine bookkeeping by scanning invoices, extracting line items, categorizing, and tagging expenses. This naturally reduces manual data entry, but it should only happen inside a platform with end-to-end encryption and SOC 2 / ISO 27001 certification. Feeding invoices into general-purpose tools can expose too much sensitive data.

Bank reconciliation and transaction matching

With secure API integrations, AI can compare bank feeds against financial statements to flag discrepancies. Done right, this cuts down hours, if not weeks, of repetitive work. But without protected integrations and audit trails, it’s risky: banking data is a prime target for attackers.

Fraud detection and anomaly spotting

Machine learning algorithms excel at identifying unusual patterns that humans might miss, from duplicate payments to suspicious vendor activity. However, building this safely requires strict privacy safeguards and enterprise-scale data analysis tools. Free AI assistants can’t deliver this level of protection.

Financial forecasting and scenario planning

AI can analyze historical data and generate predictive models for cash flow or budgeting. In enterprise systems, this can be transformative. With free tools, the safe approach is to run dummy forecasts using anonymized numbers or non-existent client names. This way, you can test AI’s potential without risking exposure.

Tax preparation support

AI can pre-fill tax forms or suggest entries, eliminating repetitive tasks for tax professionals. But because tax data equals money, it’s not safe to use tools like ChatGPT for actual client returns.

Enterprise-grade AI-powered tools with compliance features are the only safe environment here. And even then, human review is non-negotiable.

Audit support

AI can sift through large volumes of structured documents, highlight missing data, and speed up the audit process. To use this responsibly, every flagged item needs an audit trail: showing what AI spotted, how it was reviewed, and who signed off.

Client advisory insights from financial data

For advisory work, AI agents for business automation can generate dashboards, run predictive analytics, and provide valuable insights into potential expense management scenarios. But because this involves sensitive accounting data, it should only be done in trusted, enterprise-grade accounting software. Free tools can’t guarantee compliance or data security.

And further, platforms like Luzmo IQ allows accountants to explore these insights interactively, turning raw numbers into visual intelligence that clients can easily understand.

Checklist: How to use AI in accounting

Before embedding AI into your workflows, set a few ground rules. These practices keep your firm compliant and make sure you’re getting real value from artificial intelligence.

- Always anonymize client data before AI use, even on 'safe' platforms. Scrubbing names and identifiers doesn’t cost you anything but buys peace of mind.

- Stick to enterprise-grade, compliant systems when handling confidential data. Consumer-grade apps aren’t designed for secure accounting processes.

- Keep a human in the loop for validation. AI can automate repetitive tasks and even identify patterns in relevant data, but only professional review guarantees a reliable outcome.

- Document all AI-assisted outputs. If AI drafts a report or flags anomalies, keep a record of what was generated and how it was reviewed. This helps during audits or client disputes.

- Train teams on acceptable use. Many firms face a skills gap as staff experiment with tools without understanding compliance risks. Clear training reduces mistakes.

- Update governance policies regularly. As AI trends evolve, your rules for implementing AI and integrating AI into accounting must evolve too.

With clear policies in place, AI becomes a reliable partner for accountants for years to come.

Will AI replace accountants?

No, AI won’t replace accountants. It helps by automating routine tasks, but the profession still relies on human judgment and client trust.

We explored this question in detail on our blog, where we asked accountants and business professionals how they feel about AI’s role.

Read more here: Will accounting be replaced by AI?

Conclusion

AI isn’t here to replace accountants. Its role is to assist by taking on routine work through tools like robotic process automation and natural language processing, leaving more space for client service and deeper analysis. Used responsibly, it strengthens trust while delivering measurable financial outcomes and tangible cost savings.

AI can highlight patterns in accounting data, surface insights, and support strategic analysis that would otherwise be time-consuming. But technology alone isn’t enough. Accountants who combine professional judgment with growing AI expertise will be the ones ready for tomorrow’s tools and for clients who expect smarter ways of working.