Accountancy firms in the UK are entering 2026 with a mix of optimism and caution. Rising costs, talent shortages, and regulatory changes are still putting pressure on margins, even as demand for advisory work and technology-driven solutions grows. The profession is shifting from a compliance-first model to one where advisory, tech strategy, and talent management are just as critical. Below is a snapshot of where firms stand now, and what that means for the year ahead.

Economic environment

- 98% of firms report inflation and interest rates hit their business in 2023/24. Cost pressures remain unavoidable.

- 63% cite reduced profitability due to rising costs. Margins are squeezed, even with revenue growth.

- 99% say clients are also hit by higher costs; 60% of clients are being burdened with asset price rises, 55% with financing difficulty, and 53% with lower investment returns. Clients’ financial strain feeds directly into accountants' workloads.

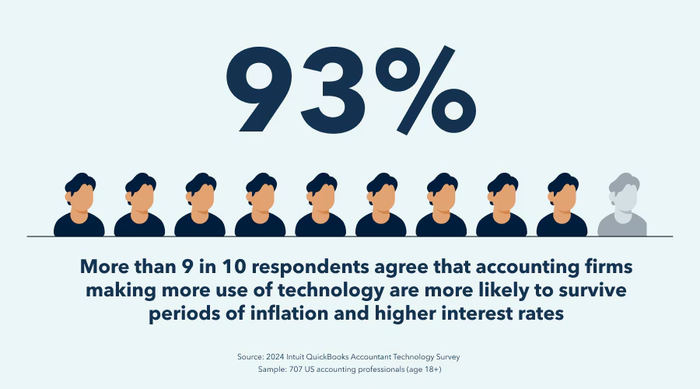

- 93% agree that tech adoption helps firms survive inflationary periods. Tech is framed as a resilience strategy.

- 92% say tech-advanced clients are better prepared for inflation/interest rate shocks. Tech-savvy clients will become more attractive to work with in 2025.

Client services

- 81% of accountants grew client lists in 2023/24, with an average 24% expansion. Demand is strong despite staffing constraints.

- 68% say clients needed more financial management support, up from 67% last year. Client reliance on accountants as finance partners keeps rising.

- 69% say clients needed more tech management support. Advising on client tech stacks is now part of the accountant's role.

- 47% of an accountant's time is now spent on advisory work. Advisory is no longer secondary; it’s half the job.

- 35% say the shift to advisory has been the single greatest positive change in the last 5 years. Industry identity is evolving rapidly.

Fee income and productivity

- Median fees per fee earner were £95,000 in 2023, an 8% increase from 2022 but still behind inflation over the same period. For UK accountants in 2025, this shows that raw growth figures can mask productivity pressures once inflation is considered.

- Median fees per fee earner varied by firm size: large firms £108k, medium £90k, small £83k. In 2025, larger firms are better positioned to attract higher-value work per staff.

- Median fees per equity partner reached £901,000 in 2023, a 13% rise from 2021. This suggests owners have seen stronger income growth than employees, which may shape expectations around firm structure.

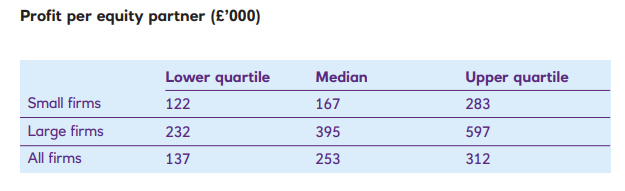

- Median fees per equity partner (PEP) grew 7% in a single year from £237k in 2022 to £253k in 2023. Earnings at the partner level are rising faster than inflation-linked salary growth.

- Audit and assurance now represent 43% of total work; accounts preparation 30%; tax 21%; advisory and restructuring combined only 6%. Compliance-heavy areas still dominate, which could limit advisory expansion unless firms shift their mix.

- The top practice area was audit and assurance (43% of firms), followed by accounts work (30%). Demand for assurance continues to climb, giving firms scope to refocus resources there.

- Tax and restructuring were reported as the weakest areas by 29% of firms. In 2025, accountants may need to diversify advisory services to avoid over-reliance on slowing segments.

- Bookkeeping and payroll together made up nearly 30% of the service mix (15.8% + 13.2%) in 2023/24. For 2025, compliance-linked recurring services still underpin stability, even as advisory grows.

- Big Four UK audit firms saw total fee income rise 11.1% in 2023, while non-Big Four firms grew 13.2% (down from 18.5% in 2022). Growth outside the Big Four is cooling, but smaller firms are still increasing their share of the market.

- Audit fee income jumped 19.5% for the Big Four in 2023; non-Big Four saw 23.2% growth. Demand for audit remains strong across the board, giving firms confidence to expand capacity.

- Average audit fee per Responsible Individual (RI) reached £2.21m in 2023, up 12% from 2022. Higher billing per auditor shows continued pressure on audit staff and reinforces the value of senior expertise.

- ESG services grew to 4.5% of the service mix, up slightly from prior years. A small but growing niche. 2025 firms can treat it as a new revenue stream bundled with audits.

- Only 3.5% of firms reported they don’t run CAS. Advisory has become almost universal, so firms not offering it in 2025 risk looking behind.

- Firms are rethinking pricing models for transparency and predictability. In 2025, subscription-like fee structures may become more common in UK practices.

Margins and profitability

- People costs dropped from 67% to 64% of earned income between 2022 and 2023. Tighter cost control has directly improved core margins.

- Core margins improved to 36% in 2023, up from 33% in 2022. This marks the best profitability level since before the pandemic.

- Large firms reported 40%+ core margins, compared with 33% for small practices. Bigger scale gives larger practices more room to absorb wage inflation.

- Median gearing (fee earners per partner) was 10, rising to 13 in large firms. Higher gearing is linked with better profit outcomes, pointing to structure as a profit driver.

- Median profit per equity partner (PEP) hit £253,000 in 2023, up 21% from £209,000 in 2022. Owners have benefited from better margins, showing how small efficiency gains translate into strong returns.

Lock-up and working capital

- Median lock-up was 105 days in 2023, up from 92 days the year before but down from 118 days in 2019. Progress has been uneven, so in 2025, firms still need to keep a close watch on cash collection cycles.

- Median debtor days stood at 66, rising from 59 in 2022. For many firms, late payments remain a drag on liquidity.

- Median WIP days were 34, with large firms at 41 and small firms at 26. Smaller firms may be managing their billing cycles more tightly than larger ones.

- Lock-up length split: top quartile firms achieved under 85 days, bottom quartile exceeded 135 days. Some firms in 2025 are running almost two months “faster” on cash cycles than others.

- Top quartile debtor days were 52, bottom quartile 88. Billing discipline clearly separates top performers from the rest.

Finance and funding

- Median borrowing stood at 31p per £1 of partner capital, with small firms slightly higher at 36p. In 2025, most firms still have unused lending capacity, which could support growth or technology investment.

- Borrowing levels by firm size: small firms median 36p debt per £1 partner capital, large firms 25p. Smaller firms lean more on borrowing to fund growth.

- One-third of firms facing tax basis reform expected to manage it through lock-up improvements, while two-thirds planned a mix of new borrowing and partner capital. Resilience in funding strategies will matter as tax reforms reshape cash flow.

- Two-thirds of firms expect to use borrowing and partner capital to handle tax basis reform. This highlights how regulatory changes can alter funding mixes.

- M&A activity is set to rise, with private equity playing a growing role. Scaling up through deals is becoming a normal path for mid-tier firms in 2025.

- Consolidation is seen as a response to the need for diversification. Firms are expanding service portfolios to avoid reliance on single income streams.

Technology and investment

- Average projected spend on accounting tech in 2024/25 is $24,000 per firm. Tech budgets are now material line items, not side projects.

- Over 75% of firms report increased tech spending, mainly in AI and automation. Tech budgets are a standard expectation in 2025.

- Efficiency and growth are the main drivers of AI/automation adoption. Firms see new tools as both a cost reducer and a growth enabler.

- 43% of firms said practice management systems are their top IT investment priority. Core system upgrades remain a bigger focus than AI, even in 2025.

- 43% cite practice management systems as #1 tech spend, but 19% say document management, and 16% CRM/client portals. Firms are gradually broadening IT investment beyond compliance tools.

- Software investment priorities differ by firm size. Large firms lean more into process automation and analytics. Small firms prioritise practice management and engagement software. In 2025, the split shows small firms chasing efficiency while big ones focus on deeper insights.

- 23% of firms faced more than four cyberattacks in 12 months, and 59% experienced at least one. Cyber risk is widespread, which makes resilience planning a must-have.

- 62.7% of firms now run a hybrid (desktop + cloud) model, up sharply from 2023. Hybrid is the new norm, with full-cloud still a minority. UK accountants in 2025 likely have to balance both.

- About 47% of firms plan to move engagement management to the cloud within two years (23.7% in 12 months, 24.1% in 13–24). Engagement processes will be the next “all-cloud” function by 2026.

- Excel is still the most common BI tool at 42.4%, despite years of BI growth. For 2025, comfort with Excel persists, but hybrid use with BI dashboards is a stepping stone.

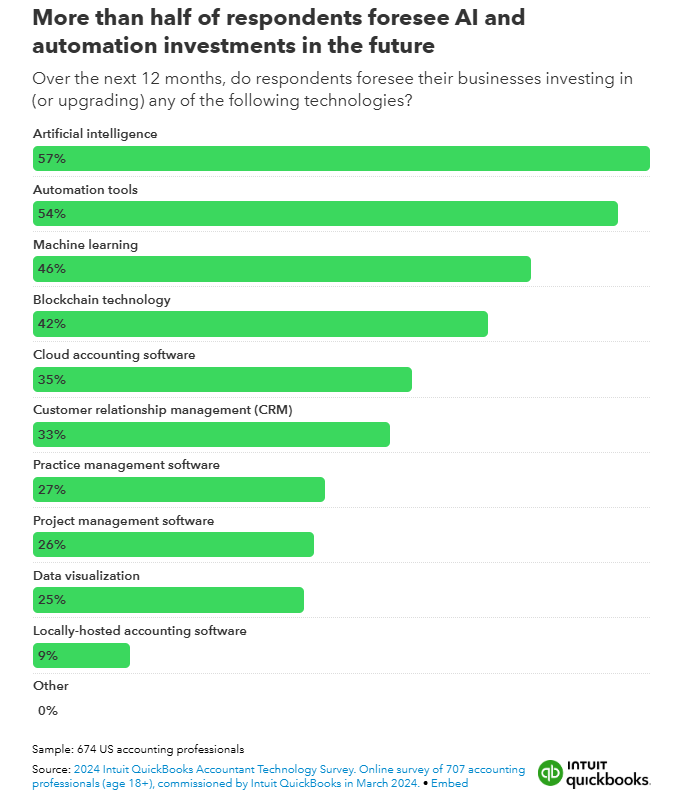

- 57% plan to invest in AI tools, 54% in automation, both up from 48% in 2023. AI and automation are now mainstream spend priorities for 2025.

- Only 10% of firms said AI is their biggest investment focus. Despite the hype, accountants are taking a cautious stance on AI adoption.

- Only 10% ranked AI as top spend, but 41% say they are “experimenting.” In 2025, firms may still be cautious, focusing on workflow instead of flashy AI.

- 16% of firms use GenAI extensively, 28.9% a little. This split shows experimentation is giving way to structured adoption in 2025.

- 32.9% of firms are still exploring GenAI. This “wait-and-see” group in 2024 could turn into late adopters or cautious users by the end of 2025.

- 98% have used AI in client-facing work over the past 12 months. AI has moved from trial to everyday practice.

- Top client AI uses: data entry (69%), fraud detection (51%), real-time insights (47%). Time savings and risk detection are the clearest wins.

- 98% have used AI internally for firm operations. AI is not only for clients, it’s transforming back-office tasks too.

- Top internal AI uses: portfolio management (65%), client comms (54%), invoicing/payments (53%). Routine admin is increasingly automated.

- Top GenAI time-savers: drafting docs (32%), data analysis (28%), brainstorming ideas (19%), summarising long texts (18%). These align directly with busy season tasks, giving 2025 adopters practical relief.

- 99% of AI adopters report following formal ethics guidelines; 66% notify clients formally. Ethical frameworks are becoming standard practice in 2025.

- Biggest AI concerns: data privacy (31%), accuracy (21%), costs (21%), job replacement (9%). The real worry is trust and compliance, not redundancy.

- 51% of firms identify as early adopters of digital tools. Early adoption is moving from fringe to majority behaviour.

- 95% agree that a willingness to learn new tech is as important as traditional accounting skills. Adaptability is as valued as technical training in 2025.

Outsourcing

- 98% outsourced at least part of their work in the past 12 months. Outsourcing is near-universal in the profession.

- Top outsourced functions: GL & transaction management (62%), AP/AR (50%), financial statements (42%). Firms are freeing compliance time first.

- 65% say outsourcing improves scalability, 56% risk management, 51% efficiency, 46% resource reallocation, and 39% accuracy. Multiple gains make outsourcing hard to ignore.

- 94% agree that outsourcing can drive profit growth by freeing capacity for advisory. Outsourcing is now viewed as a growth tool, not only a cost-cutting tactic.

Future outlook and workforce

- 91% of firms were optimistic about the future despite inflation. Confidence remains high going into 2025, though optimism will be tested by talent shortages.

- 94% report hiring challenges, up 8pp from last year. The talent crunch is worsening into 2025.

- 78% of firms said recruitment and retention are their biggest concern. Accountants entering 2025 will need to keep their people strategy front and center.

- Hiring/retention challenges dropped from 93% (2023) to 88% (2024). Slight easing, but the issue hasn’t disappeared. Firms will still chase scarce talent in 2025.

- Recruitment pressure is highest in mid-tier firms (85% citing concern), versus 70% of small firms. Mid-sized practices may feel most squeezed in 2025.

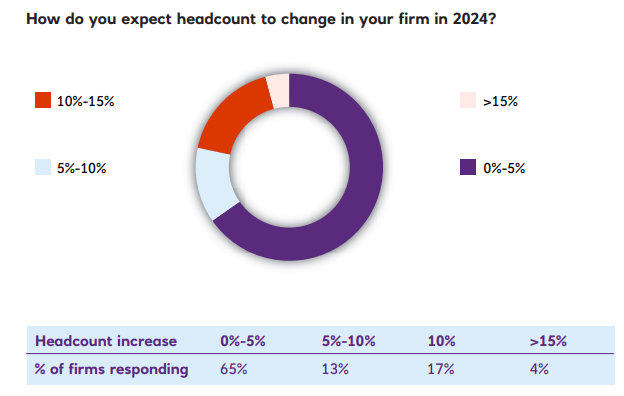

- 65% of firms expect headcount growth of up to 5% in 2024/25. Firms are planning to expand, but this depends on solving recruitment challenges.

- Upskilling staff is the top response at 32.2%; fewer firms (16.8%) chose offshoring. The training-first strategy shows firms prefer to strengthen their core teams for 2025.

- 99% say they’ll prioritise introducing the latest tech to attract and retain talent. Tools double as recruitment incentives.

- 98% agree that alternative CPA licensure pathways can prepare new entrants effectively. Calls for flexible entry routes are gaining momentum.

- Hybrid work patterns: 57% of firms said two home days per week is the most common setup. The “balanced hybrid” model looks set to remain the norm for accountants in 2025.

- Hybrid work itself was listed by 9.6% as the biggest challenge. Managing staff expectations around hybrid policies remains an ongoing balancing act.

- Hybrid arrangements differ by firm size: small firms more often mandate office-first; large firms lean on two-days-home norms. Hybrid is not uniform; staff expectations will vary by employer.

- Flexible working, career development, and incentives are reshaping workforce strategies. In 2025, talent retention depends on how firms package careers, not only salaries.

- The hunt for staff is tied directly to retention models, with flexible setups leading the way. Accountants entering the profession expect a balance between growth and personal time.

- New laws & regulations ranked as #1 challenge by 16.2% of firms, edging out tech adoption (15.4%). In 2025, compliance shifts (like UK tax reforms) will top leadership agendas.

- Virtual client communication is named a top challenge by 11.7%. Even in 2025, remote client care is not yet frictionless, showing space for tool and process upgrades.

Human skills

- 94% agree that soft skills are as important as accounting skills. Human connection remains a differentiator.

- 99% rank critical thinking as the most valuable soft skill. Analytical judgment is irreplaceable even in an AI era.

Diversity, ESG, and culture

- Just over a quarter of firms (28.5%) said they aren’t pursuing any ESG initiatives. By 2025, this gap may look like a weakness as clients expect ESG reporting.

- 36% of firms already invested in green energy, but 32% “still considering.” ESG adoption is fragmented and will likely grow under client pressure in 2025.

- 36% of firms had invested in green energy, 32% were still considering, and 36% had no plans. ESG remains a split priority, which could become a differentiator this year.

- Large firms are leading in environmental impact reduction and governance initiatives. ESG is moving from rhetoric to measurable actions, especially in bigger practices.

- Sustainability alignment is climbing the agenda, making ESG part of mainstream reporting. Clients will expect accountants to mirror the standards they advise on.

- Only 25% of firms currently pursue ESG advisory work for clients. Advisory firms that build ESG packages in 2025 could stand out.

- 53.7% of firms already implement DEI measures, and 19.1% are planning to introduce them. Over 70% of firms could have DEI policies visible to candidates.

- 27.2% still do not have DEI initiatives and don’t plan to start. This risks harming recruitment in a tight 2025 talent market.

- 87% of firms ranked DEI as at least a moderate priority, with 26% making it a top priority. Clients and recruits in 2025 will likely expect more than “moderate” progress.

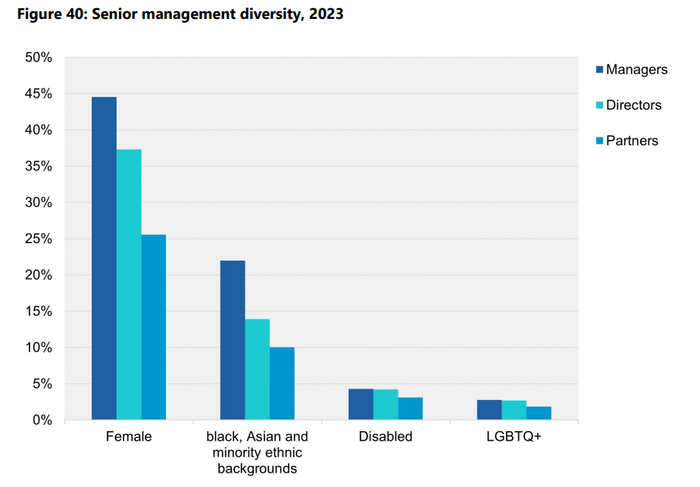

- 43% of firms said at least half of qualified fee earners are female, but only 19% had 30%+ female partners. The leadership gap is still wide.

- 43% of firms said over half of their qualified fee earners were female, but no firms had more than 50% female equity partners. Progress is visible at entry and mid-levels, but ownership diversity remains limited.

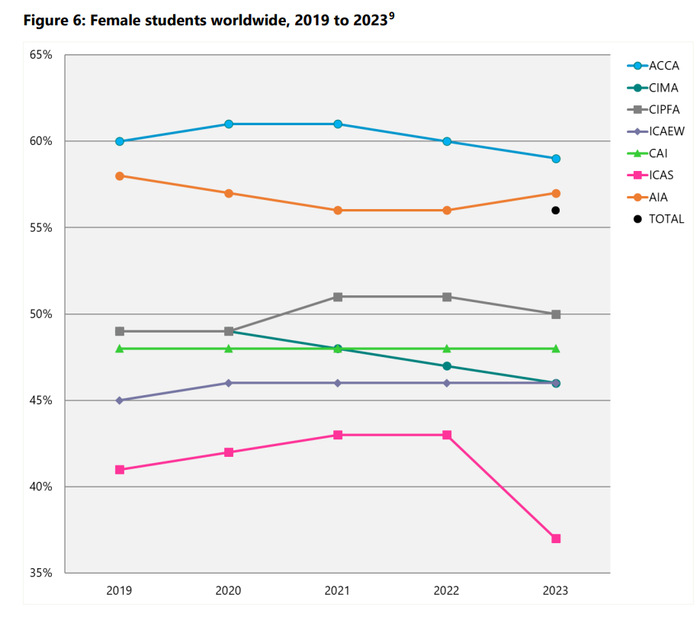

- 40% of members worldwide are female, with ACCA showing the highest proportion. Representation is improving, but leadership numbers still lag.

- All accountancy bodies collect diversity data on at least seven of the nine protected characteristics; many also track socio-economic background. Data collection is broadening, laying the groundwork for accountability in 2025.

- At PIE audit firms, data is tracked on gender, ethnicity, disability, and LGBTQ+ in senior management. Clients and regulators in 2025 can expect progress, not just measurement.

Membership and students

- Over 405,000 members in the UK & ROI in 2023, up 1.9% year-on-year; 616,000+ worldwide members (up 1.7%). Membership growth shows the profession is still expanding steadily in 2025.

- 155,000 students in the UK & ROI in 2023, slightly down 0.2%; 585,000+ students worldwide, up 0.1%. Student intake is stabilising after declines in 2022, but growth is patchy across bodies.

- Worldwide student total 585,441, flat compared with 2022. Globally, accountancy student numbers may have plateaued.

- ICAEW is the largest body in the UK & ROI with 141,561 members in 2023, followed by ACCA (113,423). For 2025, ICAEW and ACCA dominate UK membership pipelines.

- ACCA has 113,000+ UK members and 72,000+ students, the largest share among bodies. ACCA continues to dominate, meaning many future accountants will come through its routes.

- Student growth split: ICAEW up 8.5% in 2023, CIMA down 7.2%, CIPFA down 7.8%. Growth is uneven: some bodies are struggling to attract new entrants.

- 56% of students worldwide were female in 2023, compared with 40% of members. Gender balance is shifting in the pipeline, which could change firm leadership profiles in future years.

- 76% of students are aged 34 or under; the largest group of members is aged 35–44 (28%). The profession is maintaining a relatively young intake, but member demographics are ageing.

- AAT student numbers dropped 17.7% in the UK in 2023, but members grew 3.1%. Entry-level training routes are shrinking, but qualified technician membership is holding firm.

- Conversion to membership dropped 5.9% in 2023 vs 2022. Transition from study to qualification is getting harder.

Sectoral employment

- Industry & commerce employs 54% of members worldwide; only 3% of ACCA students are in practice, compared with 86% of ICAS students. Training routes differ sharply between qualifications.

Audit regulation and quality

- The number of registered audit firms fell from 5,127 in 2019 to 4,038 in 2023 (21% drop). Ongoing consolidation limits audit supply in 2025.

- New applicants to become registered audit firms rose 9.6% in 2023, after a sharp fall the year before. There is some fresh interest in audit registrations despite the overall decline.

- Monitoring visits by RSBs in 2023 covered 21.6% of firms, consistent with the 6-year statutory cycle. Most firms can expect at least one regulatory visit before 2030.

- Complaints about auditors up to 171 in 2023, the highest in three years. Oversight pressure is not easing.

- Number of registered audit firms dropped to 4,038 in 2023, down from 5,127 in 2019. Consolidation continues, shrinking the pool of statutory auditors in the UK.

- Audit Quality Review (AQR) inspections fell to 133 in 2023/24, from 152 two years earlier. Fewer inspections may reflect resource limits, but high-profile firms remain under close watch.

Body resources

- ACCA income £246m in 2023, the highest of all bodies; ICAS has the highest per-member income at £707. Bigger bodies dominate the total scale; smaller ones earn more per head.

- ICAEW staffing up 11% in 2023; overall accountancy body staff count up 4.8%. Professional bodies themselves are growing operations in 2025.

Over to you

UK accountancy is in transition. Firms are still navigating inflation, tighter cash cycles, and hiring challenges, but they are also becoming more technology-driven, advisory-focused, and structurally efficient. The practices that thrive in 2025 will be those that double down on efficiency, invest in tech that supports people and clients, and stay flexible enough to capture new revenue streams. The profession may look different in a few years, but for now, the foundations for stronger, more resilient firms are being laid.