You're doing the work. Customers are interested. The business has legs, but without capital, it stalls. In 2025, over 50% of small business owners say funding is the biggest thing holding them back. This guide walks you through how to get a small business loan: from choosing the right type to actually securing the money.

Should you apply for a small business loan?

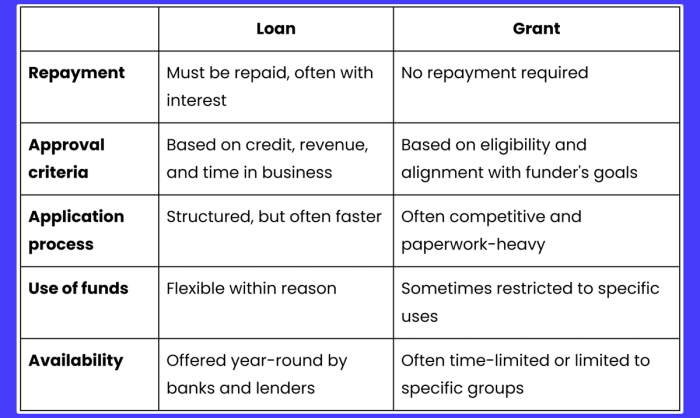

Before jumping in, take a moment to weigh up your options. A loan isn’t the same as a grant, and it comes with responsibilities that might not fit every stage of your business.

Loan vs grant: key differences

When a loan might make sense:

- You have a clear plan and timeline for using the funds

- You can handle the repayments without straining your cash flow

- You're investing in something that will generate a return (e.g. equipment, new hire, expansion)

When to think twice:

- You're already struggling to stay afloat month to month

- You’re not sure how much you really need — or why

- Your business finances are messy or disorganized

Taking on a loan can fuel serious growth, but it’s not free money. Use it when the math works in your favor.

Types of small business loans

A loan is a financial tool designed to support a clear business goal. When used with intention, it can unlock opportunities like expansion, equipment upgrades, or bridging cash flow gaps. Here’s a look at the most common types of small business loans — and when they make the most sense.

#1 Term loans

A term loan gives you a fixed amount of money upfront, which you repay over time with interest, usually in monthly installments. It’s best suited for larger, one-time investments like opening a new location, upgrading equipment, or launching a new product line.

This type of loan is ideal if you have a specific goal in mind, a predictable revenue stream, and you want to lock in fixed repayment terms. The stability can help with planning, and the funding amount is often higher than other types of financing.

Example: Borrow $50,000 and repay it monthly over 5 years.

When it’s useful:

- You know exactly what you need the money for

- You’re making a long-term investment in your business

- You can comfortably cover fixed monthly repayments

Some US lenders that offer term loans:

- Bank of America – Loans from $10,000 with fixed monthly payments and competitive rates

- Funding Circle USA – Loans from $25,000 to $500,000, terms from 6 months to 7 years

- OnDeck – Short- and medium-term loans with funding in as little as 1–3 days

Some UK lenders offering term loans:

- HSBC UK – Fixed-rate business loans with terms from 1 to 10 years

- Lloyds Bank – Loans with flexible repayment periods up to 25 years

- iwoca – Online lender offering loans from £1,000 to £500,000, terms of 1 to 60 months

#2 SBA loans (US) / Start Up Loans (UK)

These are government-backed loans designed to make business funding more accessible.

In the United States, SBA loans are issued by approved lenders but guaranteed by the Small Business Administration. This reduces the lender’s risk, making it easier for small businesses to qualify, often with lower interest rates and longer repayment terms than traditional loans.

The most common SBA loans:

- 7(a) loan – for general working capital or expansion

- 504 loan – for real estate or major equipment

- Microloans – up to $50,000, ideal for small projects or early-stage businesses

The application process can be lengthy and document-heavy. Expect to submit a detailed business plan, financials, and sometimes a down payment or personal guarantee.

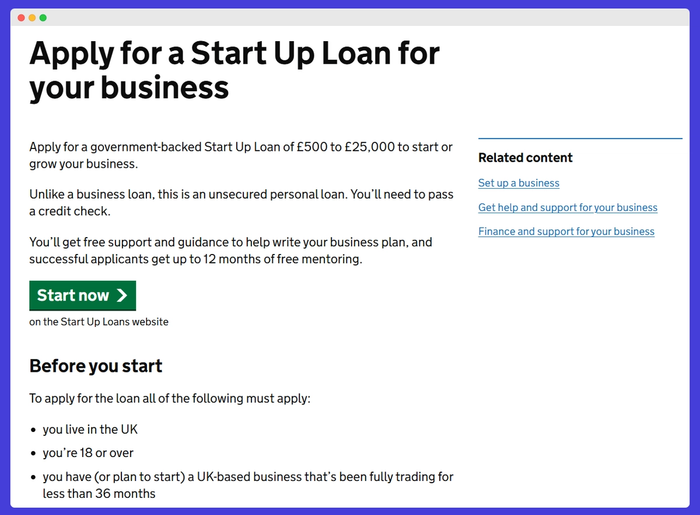

In the United Kingdom, the Start Up Loans scheme provides £500 to £25,000 in unsecured personal loans to help new businesses get off the ground or scale early operations. To qualify, you must be 18 or older, based in the UK, and run a business that has been trading for less than 36 months.

Loans come with a fixed 6% interest rate and repayment terms of 1 to 5 years. There are no fees to apply and no penalties for early repayment. What makes this scheme especially valuable is the added support: recipients get help with their business plan and up to 12 months of free mentoring.

Best for:

- First-time founders looking for affordable, structured funding

- Small business owners who want both capital and hands-on startup guidance

#3 Line of credit

A business line of credit gives you flexible access to funds — you only borrow what you need and pay interest on the amount used. It’s ideal for covering seasonal dips or managing unexpected expenses without committing to a full loan.

It’s often perceived as a more powerful version of a business credit card, with higher limits and better terms.

Best for:

- Businesses with fluctuating income

- Owners who want access to capital on demand, not all at once

Some US companies offering lines of credit:

- BlueVine – Offers revolving lines of credit up to $250,000, with fast approvals and flexible repayment terms.

- Fundbox – Provides lines up to $150,000, with funds often available by the next business day.

- Wells Fargo – Offers secured and unsecured business lines starting at $5,000, designed for working capital needs.

Some UK companies offering lines of credit:

- Fleximize – Offers flexible facilities with no early repayment penalties, ideal for managing short-term cash flow.

- Capify – Provides revolving credit lines up to £150,000, well-suited for small and mid-sized businesses.

- Liberis – Uses future revenue to offer funding, making it a fit for retail or service-based businesses with consistent card sales.

#4 Microloans

Microloans are small-scale loans — typically under $50,000 — designed for early-stage businesses, freelancers, or entrepreneurs who may not yet qualify for traditional financing. They're offered by nonprofits, community lenders, or government programs.

Unlike term loans, microloans are more accessible, even if your business is new, your credit score isn’t perfect, or you don’t have collateral. They’re especially useful for low-risk purchases like equipment, supplies, or launching your first product.

That said, the tradeoff is often higher interest rates and shorter repayment terms, making them better for small, strategic investments, not long-term financing.

When a microloan makes sense:

- You’ve been turned down by a bank

- You only need a few thousand dollars/pounds to get started

- You’re building a credit history for your business

- You’re part of an underserved community

U.S. providers:

- Accion Opportunity Fund – Offers microloans from $5,000 to $100,000, with a focus on minority, women, and veteran entrepreneurs.

- SBA Microloan Program – Loans up to $50,000, provided through local intermediaries. Often bundled with free business training and support.

- Kiva US – Provides interest-free loans up to $15,000, crowdfunded by individual lenders who support small business owners directly.

U.K. providers:

- Start Up Loans (British Business Bank) – Government-backed loans from £500–£25,000, paired with free mentoring for 12 months.

- Fredericks Foundation – Supports entrepreneurs rejected by traditional lenders, focusing on disadvantaged or underserved applicants.

- Let’s Do Business Group – Offers microloans to businesses across the UK, especially those ineligible for bank loans.

#5 Other funding options

Not every small business fits neatly into a standard loan category. Depending on your revenue model or needs, alternative financing might make more sense. These options are more specialized — and often faster to access — but usually come at a higher cost.

Equipment loans

Perfect if you’re buying high-value tools, machinery, or vehicles. These loans are secured by the equipment itself, which means you may qualify even with a limited credit history.

- Good fit for: restaurants, construction, manufacturing

- Watch for: depreciation — if the gear becomes outdated, you might still be paying it off.

Invoice financing (a.k.a. invoice factoring)

Get an advance on your unpaid invoices — often up to 90% of the value — and receive the rest (minus fees) when your client pays.

- Good fit for: B2B companies with long payment terms

- Watch for: fees can climb quickly, especially if your clients are slow to pay.

Merchant cash advances

You receive a lump sum upfront and repay it via a percentage of your daily card sales. Fast access, but costly.

- Good fit for: retail or hospitality businesses with consistent card revenue

- Watch for: effective APRs (annual percentage rates) can be well over 50% — this is one of the most expensive forms of funding.

These tools can help when you need quick capital or don’t qualify for traditional loans. But they should be used strategically and sparingly — not for long-term needs or when you're already cash-strapped.

Check this out - the ultimate guide to small business funding

How to apply for a loan – step by step

Applying for a small business loan can feel overwhelming, especially with rejection rates hovering around 1 in 3. But when you break it down, the process becomes much more manageable. Here’s how to get through it – prepared and with your best foot forward.

Step 1: Define how much you need and why

Start with clarity: how much money do you need, and what exactly will you use it for?

Whether it's £15,000 for inventory, $30,000 to expand your team, lenders want to see you’ve done the math. A specific use case improves your odds of approval and helps you choose the right loan product.

Step 2: Research lender options

Banks. Online lenders. Government-backed programs. Nonprofits.

Each lender type comes with different expectations, rates, and application speeds. Banks are stricter but offer better terms. Online lenders are faster, but often pricier. Local development agencies might be more flexible if you’re a good fit.

Compare not just percentage rates, but also term lengths, early repayment fees, approval times, and paperwork demands. If you already bank somewhere, check their business loan offers first.

Step 3: Check eligibility

This is where most applications fall apart – not because the business isn’t strong, but because it’s not what the lender wants.

Here’s what most lenders consider essential:

Credit score

Your personal credit score (and business credit, if available). A score above 680 is ideal, but some online lenders accept 600+.

Bring: Your latest credit report, ideally from Experian, Equifax, or TransUnion.

Time in business

Many banks prefer 2+ years; some online lenders accept 6–12 months. Startups? Try microloans or personal credit-based products.

Bring: Business registration or incorporation documents.

Revenue and cash flow

Can you afford repayments? Lenders want to see consistent income and a stable runway.

Bring: Bank statements (6–12 months), tax returns (1–2 years), and profit & loss statements.

Collateral or personal guarantees

If the loan is secured, you’ll need to list what you’re offering.

Bring: Asset documentation or a signed guarantor statement if applicable.

Use of funds

Be clear about how you’ll use the loan — lenders want purpose, not guesswork.

Bring: A short business plan or note explaining your funding goals, timelines, and projected outcomes.

Step 4: Strengthen your application

This step’s optional – but powerful.

If you’re not in a rush, take time to boost your credit score, organize your financials, or secure a contract that improves your revenue. Even small changes – a 30-point credit bump or a tidy balance sheet – can unlock better offers.

Also: if you can offer a guarantor or asset, mention it up front.

Step 5: Apply with confidence

Now you’re ready to apply.

Complete forms carefully. Double-check for missing details. Upload your documents and be ready to answer questions about your business and goals.

After submitting, stay responsive. Lenders might request extra info, and slow replies can stall or cancel your application. If you apply to multiple places, keep a tracker of who’s responded and what they’ve offered.

Step 6: Review the offer before you accept

Approval doesn’t mean ‘yes’ right away.

Look at the APR, monthly repayment, repayment term, and total cost. Watch for fees like origination charges or prepayment penalties. Ask questions if anything’s unclear.

You don’t just want a loan. You want a loan that fits your business without choking its cash flow. Make sure this one does.

Tips for success when applying for a small business loan

Getting approved for a loan isn’t just about having the right paperwork. It’s about showing lenders that you understand your business, have a plan for growth, and know how to manage money responsibly.

- Start with a focused business plan — not pages of filler, but a simple, confident outline. Explain what the loan will fund, how it’ll help your business grow, and how you’ll pay it back. A lender doesn’t need a pitch deck. They need to know the numbers add up.

- Speaking of numbers — know yours. If you can’t clearly state last month’s revenue, your profit margin, or how much debt you already carry, you’re not ready to borrow. Get familiar with the key figures and have a short explanation ready for any dips or irregularities.

- Then, compare offers carefully. It’s easy to be drawn to the lowest interest rate, but what really matters is the total cost of the loan. Look out for fees, repayment flexibility, and whether the terms match your business model. Sometimes the better option isn’t the cheapest on paper.

- Watch for red flags. If a lender promises approval without reviewing your documents or pressures you to decide fast, pause. Reputable lenders want to verify your business — and that’s a good thing.

- Finally, treat the process seriously. Use a professional email, submit clear documents, and be prompt with replies. First impressions matter. Even small things — like how organized your application is — can signal whether you’re ready to handle a loan.

And once you’re approved, don’t just celebrate — plan. Be intentional with the funds, track where every dollar goes, and check in monthly to stay on top of repayment.

For example: if you’re using a $20,000 loan to launch a new product line, break it down: $10,000 toward inventory, $5,000 for marketing, $3,000 for packaging, and $2,000 for unexpected costs. Keep a simple spreadsheet (or use your accounting tool) to log every expense. Set a reminder each month to review how you’re pacing against your revenue goals and repayment timeline. This helps you stay in control — and proves to future lenders that you’re loan-ready again if needed.

Conclusion

Many small business owners hesitate to take out a loan — it can feel like a risk or a last resort. But in reality, the right loan is a tool, not a trap. It can help you invest, grow, and stay in control of your business on your own terms.

As long as you understand the numbers and choose carefully, a loan doesn’t hold you back — it moves you forward.

FAQ

There’s no one-size-fits-all number, but higher is generally better. Most banks look for a personal credit score of 680 or above. SBA-backed loans typically go to borrowers closer to 700. That said, some online lenders approve scores in the 500–600 range if other factors (like revenue or cash flow) are strong.

Yes, many small business loans are unsecured, meaning you don’t need to pledge property or equipment. This includes unsecured lines of credit and loans from many online lenders. However, most lenders will still require a personal guarantee, and some may file a blanket lien (UCC) as extra security.

Timelines vary. Online lenders often fund within 1–3 business days, while banks and SBA loans can take several weeks. SBA 7(a) loans, for example, typically take 4–6 weeks due to detailed paperwork and approvals.

Often, yes. SBA 7(a) and 504 loans usually require at least 10% from the borrower, especially for real estate or business acquisition. Startups might need to contribute more. SBA Microloans (under $50,000) generally don’t require a down payment, but they might not cover your full needs.