Digital agencies in the UK are stepping into 2026 with more momentum than ever. The numbers back it up: industry revenues keep climbing, investment is flowing in, and client demand shows no signs of slowing down. From £66.6 billion in ad spend to over 8,500 agencies competing nationwide, this sector is now a cornerstone of the UK economy, accounting for 4% of national output and employing nearly 1.7 million people.

But beyond the topline growth, the data tells a deeper story: which channels are winning, where budgets are shifting, and how agencies can position themselves for the next wave of expansion. Here’s a closer look at the stats and trends shaping the digital agency market in 2026.

Market size & investment

- £66.6bn was spent on advertising in 2024 by 3.5 million UK businesses. This shows the industry is one of the largest growth engines, with agencies at the centre of it.

- Of that spend, £42.6bn went to media, £7.4bn to agencies and production, and £16.6bn to marketing professionals. The agency share is still strong, but it also signals room to win more of the budget.

- On average, every £1 spent on advertising returns £4.11 for medium to large firms and £1.89 for smaller businesses. Even micro clients see nearly double back, making ROI a strong argument when pitching.

- Industry revenue reached £17.9bn in 2023-24, with predictions to rise at 7.7% a year for five years. Growth has been steady, proving digital agencies are not riding on short-lived trends.

- By 2025, industry revenue hit £20.4bn, growing 7.2% a year since 2019. This shows digital agencies continue to outpace traditional media.

- There were 8,509 digital agencies in 2024, up 5.1% annually since 2019. Competition is strong, but the expanding client demand keeps the market healthy.

- Revenue is forecast to rise 6.3% between 2024–25, with growth expected through 2030. Agency owners can plan long-term with confidence that budgets will not dry up.

- The wider UK agency market, including creative, PR, and performance shops, is worth £46.4bn. Digital agencies form a major slice of this bigger pie.

- The sector attracts outside capital, with £3.9bn raised in investment funding and £16.7m in Innovate UK grants. For ambitious owners, this shows investors see agencies as strong bets.

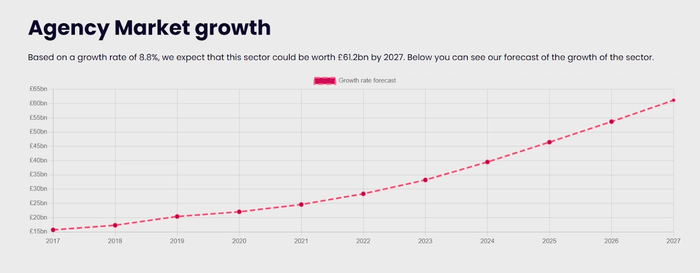

- Overall, the agency market is growing 8.8% a year and is forecast to reach £61.2bn by 2027. Few sectors in the UK economy are growing this fast, making agencies a long-term growth story.

Demand drivers

- Internet penetration is 97.8% (67.8m users), up by ~421k year over year. Your next client already lives online, so plan digital-first by default.

- 85% of the UK population is urban. Target dense local areas for faster tests, cheaper learnings, and quick scale.

- Surging internet usage keeps brands investing in online presence. This isn’t a fad, but how people research and buy.

- Clients want creative work, media buying, and real guidance in one place. If you pair execution with advice, you’re harder to replace.

Channel reach & audience mix

- 54.8m social media identities (79% of population); 80.8% of internet users use social. Social remains the broadest reach lever for performance and brand.

- YouTube ad reach ~54.8m (79% of population). Video can be treated as mass media with performance controls.

- Facebook ad reach ~38.3m (55% of population). Still a national-scale channel for consideration and DR.

- Instagram ad reach ~33.4m (48% of population). Visual commerce and creator collabs have enough reach to drive sales, not only awareness.

- TikTok ads reach 24.8m adults (45% of 18+). Short-form video is now mainstream for adults, so put TikTok in core mixes, not test budgets.

- LinkedIn members ~45m (82% of 18+). B2B targeting can cover most decision-makers, so ABM scale is real.

- Snapchat ad reach ~23.9m (35% of population). Useful for younger segments and incremental reach.

- Messenger ad reach ~26.7m (39% of internet users). Messaging placements still add cheap frequency and re-engagement.

- X ad reach ~22.9m (33% of population). Treat as a niche high-intent channel, not a primary reach vehicle.

Platform momentum (who’s rising, who’s flat)

- TikTok +9.2% YoY ad reach; +4.1% QoQ. Budget share can rise without sacrificing scale.

- LinkedIn +15.4% YoY members; +4.7% QoQ. Push B2B upper-funnel and lead gen while CPMs are still workable.

- Instagram +0.9% YoY; +2.9% QoQ. Reels keeps Instagram relevant for growth campaigns.

- Facebook +3.2% YoY; +1.5% QoQ. Stable reach supports evergreen acquisition and retargeting.

- Pinterest +14.7% YoY; +0.3% QoQ. Product discovery is improving, so do test for retail and home categories.

- YouTube -2.5% YoY (flat QoQ). Plan for steady GRPs with a creative refresh to hold attention.

- Messenger -3.8% YoY. Keep for retargeting rather than prospecting.

- X -10.7% YoY; -4.7% QoQ. Use selectively for moments and interest clusters.

Growth areas

- SEO remains the largest slice of agency services. With forecast growth of 7.4% in 2025, it’s the backbone of online visibility and a safe bet for long-term retainers.

- Display advertising is set to grow 9.4% in 2025. Pairing SEO with display gives clients both visibility and reach, creating balanced growth opportunities for agencies.

- Mobile and video formats are taking a larger share of industry revenue. Agencies that prioritise these areas can charge higher margins and meet client demand for richer storytelling.

- Social media keeps pulling spend away from TV and print. Agencies with strong social expertise will continue to win budgets that used to go to traditional channels.

- Influencer marketing was worth £828m in 2023 and is set to hit £1bn by 2026. Agencies that build creator partnerships now will secure a slice of the next big revenue stream.

- TikTok and YouTube remain advertiser hotspots, even during cost-of-living pressure. Knowledge of these platforms keeps agencies relevant and attractive to clients.

- Retail leads demand, with clothing, furniture, footwear, and jewellery brands relying heavily on online ad agencies. Specialists in retail campaigns are positioned to thrive in 2026.

- Branding (3,971 firms) and performance marketing (3,065 firms) are the fastest-scaling verticals. For agencies, these two are the clearest growth bets heading into 2026.

- Creative (2,846 firms) and e-commerce (2,633 firms) also show strong expansion. These fields remain reliable entry points for agencies that want scale.

- Other verticals include analytics, CRM, digital transformation, PR, social media, and user experience. Specialisation is spreading, giving agencies new niches to compete in and grow.

Media performance enablers (infrastructure)

- Median mobile download speed is 58 Mbps (+19.8% YoY), while fixed broadband is 123.9 Mbps (+34.5% YoY). With faster connections, agencies can confidently run HD video and interactive formats without worrying about slow delivery. To keep campaigns running smoothly, agencies should also monitor uptime and server health. Reliable infrastructure monitoring tools can help detect outages early.

- There are 88.4m mobile connections in the UK, equal to 127% of the population, and 99.4% are 3G/4G/5G capable. Always-on mobile reach is the new baseline, so agencies should plan content around true mobility and smart dayparting.

Targeting & demographics

- 87% of UK adults use social media, with men and women evenly split. This means agencies can run national campaigns without heavy overlap or wasted reach.

- The median age is 40.1, with strong cohorts in the 25–44 range. Campaigns aimed at mid-career, purchase-ready groups can drive the best short-term results.

Employment impact

- Advertising supports 1.7m jobs, or 5% of all UK employment. Agencies aren’t a side player; they’re a major employer across the country.

- 60% of roles are outside London, with the North West at 12%, the South East 11%, and Yorkshire & Humber at 8%. The talent pool is spreading, so agencies beyond the capital get a stronger base.

- London’s workforce share has dropped by 3 points since 2017, while Manchester, Leeds, Liverpool, and Sheffield gained ground. Regional hubs are now credible power centres for agencies.

- High demand for SEO, digital design, and web development skills is pushing up wages. Agencies that secure top creative talent can stand out, but need to budget for rising pay.

- Managing distributed teams efficiently is another challenge as agencies expand. Using an attendance management system helps track hours across locations, streamline payroll, and stay compliant with UK labour laws—especially as hybrid work becomes the norm.

- Revenue per employee keeps climbing. Owners can point to strong productivity to justify higher fees with clients.

- In the wider agency market, 207,621 people are employed across 16,136 companies. This is a crowded but healthy ecosystem where competition for both staff and clients is part of the growth story.

Regional distribution

- London remains the main hub thanks to its HQ concentration and talent pools. Agencies here still benefit from direct access to the country’s biggest decision-makers.

- But Manchester and Leeds are catching up fast. Regional agencies now win major accounts, proving that strong talent and client delivery matter more than postcode.

Economic contribution

- Advertising added £109bn in GVA in 2024, equal to 4% of the UK economy. This makes agencies a heavyweight part of the national picture, not a side industry.

- The sector outperformed film, TV, law, and accounting. Agency owners can confidently say their work delivers more value than many long-standing industries.

- The wider digital sector contributed £153.5bn in 2023, or 6.5% of UK GVA. Agencies sit at the heart of this digital-first economy.

- The share slipped from 6.8% in 2022, as GVA dipped 1.6% while the wider economy grew 0.4%. Agencies are not immune to headwinds, but they still lead on long-term growth.

- Between 2019 and 2023, digital GVA rose 13.7% after inflation. Even in turbulent years, digital proved itself a reliable growth engine.

- Revised data shows a 15.6% rise from 2019 to 2022, higher than first reported. The corrected trend strengthens confidence in digital-led business models.

Global position & exports

- The UK exported £17.9bn in advertising services in 2024, second only to the US. This shows agencies here compete on the world stage, not just at home.

- The UK holds the highest e-commerce share of retail sales globally, at 30% versus 24% in the US. Agencies skilled in online retail strategy have an international edge.

Major players

- WPP leads with £1.3bn in 2025 revenue. Their acquisition-led strategy highlights the advantage of scale and tech adoption mixed with global reach.

- Publicis Groupe (£861.5m) and Interpublic (£538.5m) follow. The giants dominate the top tier, but agile independents still find room to grow by moving faster and staying niche.

Subsector dynamics

- Computer programming, consultancy, and related services fell 6.7% from 2022 to 2023. Agencies tied closely to pure software may face tighter client budgets.

- Telecommunications, the second-largest subsector, grew 8.6% over the same period. Agencies that work with telco and connectivity brands can tap into the rising demand for digital infrastructure.

Competitive forces

- More businesses are bringing advertising in-house to cut costs. Agencies must stand out with deeper expertise, smarter tech, or scale that in-house teams can’t match.

- Rival sectors like PR and consultancies are moving into digital advertising. Competition isn’t agency-only anymore, so positioning and niche strength matter.

- Agencies looking for creative ways to engage communities or raise funds for client campaigns can experiment with silent auction ideas. These events are low-cost, create buzz, and double as great PR opportunities.

- Some brands go direct to Google and Meta. This squeezes agency fees and means you must prove why your skills drive better outcomes than platform self-serve.

- Buyer power is rising in a crowded market. Protecting margins means moving up the value chain. Measured strategy and integration are harder to cut than media buying alone.

Measurement & planning notes

- Ad reach ≠ active users. Platforms revise their numbers often, so report with caveats and guide clients toward trusted KPIs like lift, CPA, and ROAS.

- Social identities dropped -2.5% YoY due to methodology changes. This isn’t a collapse in usage. Cross-check with sales and web data before shifting spend.

Industry resilience

- COVID-19 slowed agency revenue when budgets were cut, but recovery was swift. The bounce back shows the industry can adapt under pressure.

- The cost-of-living crisis has tightened growth, but easing inflation is expected to lift budgets. Agencies that keep clients engaged now will ride the rebound.

- Real-time data shows agency numbers and turnover still rising. Even with broader uncertainty, agencies are proving adaptable and resilient.

- The digital sector still contributed over one in every fifteen pounds of UK GVA in 2023. Even with a dip, digital isn’t shrinking. It actually remains a heavyweight.

- Updated growth tracking shows digital has consistently outpaced the wider economy. Owners can reassure clients that digital spend aligns with where the economy itself is heading.

Practical mix guidance for 2026

- Always-on spine: Search + Meta + YouTube (reach + retargeting) to anchor scale. These form the backbone of most campaigns.

- Growth lanes: TikTok (adults), Instagram Reels, Pinterest for retail discovery, LinkedIn for B2B.

- Selective add-ons: Snapchat for youth reach; X for live moments and niche interests.

Conclusion

If you’re betting on the future of UK digital agencies, the odds look good: but only for those who can read the signals. Growth is strong, but so is competition. Clients are savvier, budgets are shifting, and the platforms themselves are changing the rules quarter by quarter.

The agencies that thrive in 2026 will use the numbers to prove value, sharpen their positioning, and carve out space in a crowded market. If you can do that, you won’t just keep pace with the industry: you’ll help define it.

![Business statistics every business owner should know [2026]](data:image/jpeg;base64,/9j/2wBDAAYEBQYFBAYGBQYHBwYIChAKCgkJChQODwwQFxQYGBcUFhYaHSUfGhsjHBYWICwgIyYnKSopGR8tMC0oMCUoKSj/2wBDAQcHBwoIChMKChMoGhYaKCgoKCgoKCgoKCgoKCgoKCgoKCgoKCgoKCgoKCgoKCgoKCgoKCgoKCgoKCgoKCgoKCj/wAARCAALABQDASIAAhEBAxEB/8QAGgAAAQUBAAAAAAAAAAAAAAAAAAECAwQFBv/EACEQAAEEAgICAwAAAAAAAAAAAAEAAgMRBCEFBhJRE3GR/8QAFgEBAQEAAAAAAAAAAAAAAAAAAgAG/8QAGhEAAgIDAAAAAAAAAAAAAAAAAAECAxESgf/aAAwDAQACEQMRAD8A6rqEGJk83DFnlvxOuvI6JSdtxsXB5qeHELTEN202AfSzmNFXW1Xftxvf2gaR1Ny2zwjMrR7/ABCeAEKGf//Z)

![Business statistics every business owner should know [2026]](https://cdn.sanity.io/images/poftgen7/production/5619faf6a65f53406d3e554c11c9e894402d4397-5760x3240.jpg?rect=5,0,5751,3240&w=300&h=169&q=75&fit=max&auto=format)